We’ve all been there—applying for a loan, a job, or even a new apartment, only to get hit with that dreaded rejection. It stings, doesn’t it? But here’s something you might not know: there’s a legal safety net in place to make sure you’re not left in the dark.

It’s called the FCRA Adverse Action Notice, and understanding it can turn that rejection into an opportunity to take control of your financial future. Stick with me, and I’ll break it down in a way that’s easy to digest.

In simple terms, the FCRA (Fair Credit Reporting Act) Adverse Action Notice is like a heads-up that businesses are required to give you when they use your credit report to make a decision that doesn’t go your way. Whether it’s turning down your credit application, hiking up your interest rate, or even rejecting your job application, if your credit report played a role in that decision, they’ve got to tell you about it.

You might wonder, “Why is this notice such a big deal?” Well, it’s all about transparency and fairness. The FCRA Adverse Action Notice ensures that you’re not just left wondering what went wrong. Instead, it gives you the power to understand why the decision was made and, more importantly, what you can do about it.

Here’s the thing—just about any business that uses your credit information to make decisions could be required to send you an Adverse Action Notice. We’re talking lenders, employers, landlords, insurance companies, and even your utility provider! If they peek at your credit report and it affects their decision, they owe you that notice.

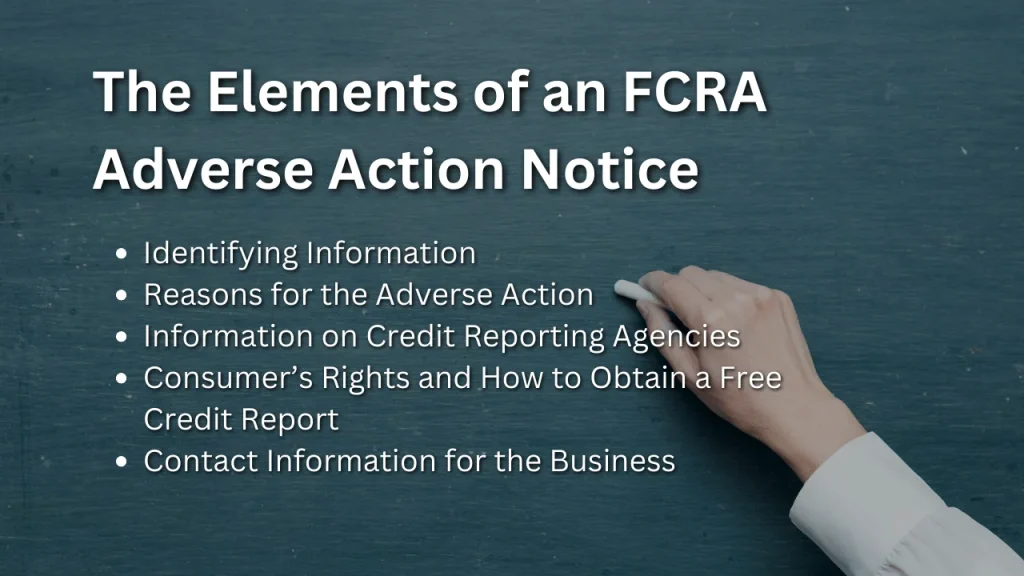

Alright, let’s get into the nitty-gritty. What exactly should you expect to find in this notice?

The beauty of the FCRA Adverse Action Notice is that it puts the power back in your hands. It’s not just about being told “no”—it’s about knowing why and what you can do next. Maybe there’s an error on your credit report that you didn’t even know about, or perhaps you can take steps to improve your credit for the future. Either way, this notice gives you the information you need to make informed decisions.

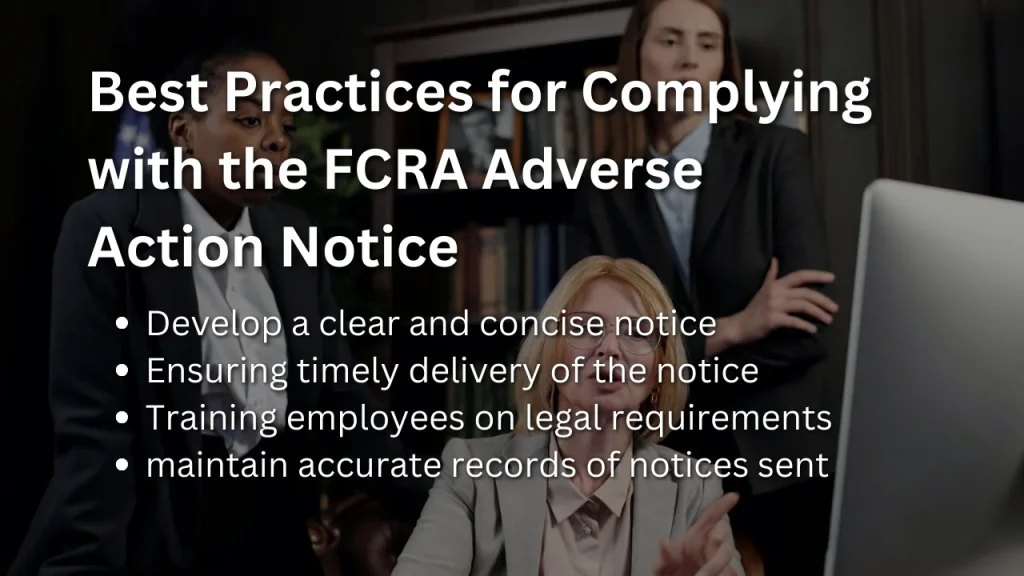

Let’s say a business doesn’t send you this notice when they should. That’s a big no-no, and it can lead to serious consequences. Regulatory bodies like the Consumer Financial Protection Bureau (CFPB) and the Federal Trade Commission (FTC) are on the lookout for these slip-ups. Businesses that don’t comply can face hefty fines, lawsuits, and a tarnished reputation.

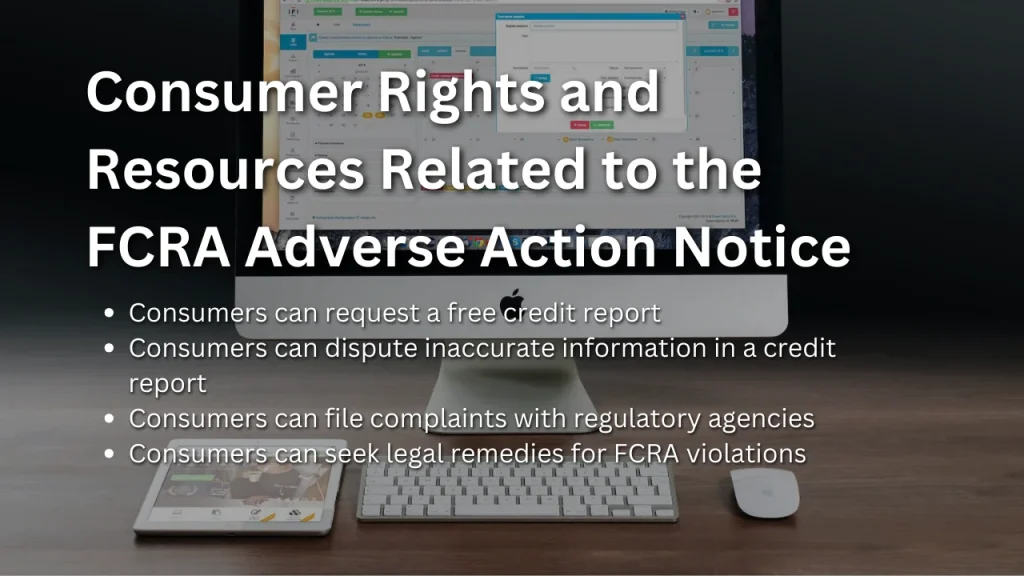

Credit reporting agencies (CRAs) are the gatekeepers of your credit information. They’re responsible for making sure the info they provide to businesses is accurate and up-to-date. If you find something fishy on your credit report after receiving an adverse action notice, you can dispute it with the CRA. They’re required to investigate and fix any errors, giving you a better shot at getting that loan or job next time around.

What exactly is an ‘adverse action’?

An adverse action is any decision by a business that negatively impacts you based on your credit report. This could be anything from denying you a loan to not hiring you for a job because of what they saw on your credit report.

Can businesses just send out a generic notice?

While some might be tempted to use a one-size-fits-all approach, the FCRA requires these notices to be specific to your situation. Generic notices can lead to compliance issues and leave you without the details you need.

How long do businesses need to keep these records?

Businesses are required to hang onto records of these notices for five years. This helps ensure they can prove compliance if regulators come knocking.

The next time you receive an FCRA Adverse Action Notice, don’t just toss it aside. This is your chance to take control of your financial situation. Review the reasons for the adverse action, check your credit report, and if needed, take steps to correct any inaccuracies. And remember, this notice isn’t just a rejection—it’s a tool for you to improve and make sure your next application is a success.

Understanding the FCRA Adverse Action Notice might seem a bit daunting at first, but it’s all about giving you the power to protect your financial future. So the next time you find yourself on the receiving end of one, you’ll know exactly what to do.